Introduction

Life is full of unexpected events. A sudden medical expense, vehicle repair, job loss, or urgent home maintenance issue can put significant pressure on your finances. Without savings set aside for emergencies, many people rely on credit cards, loans, or other forms of debt to cover these unexpected costs.

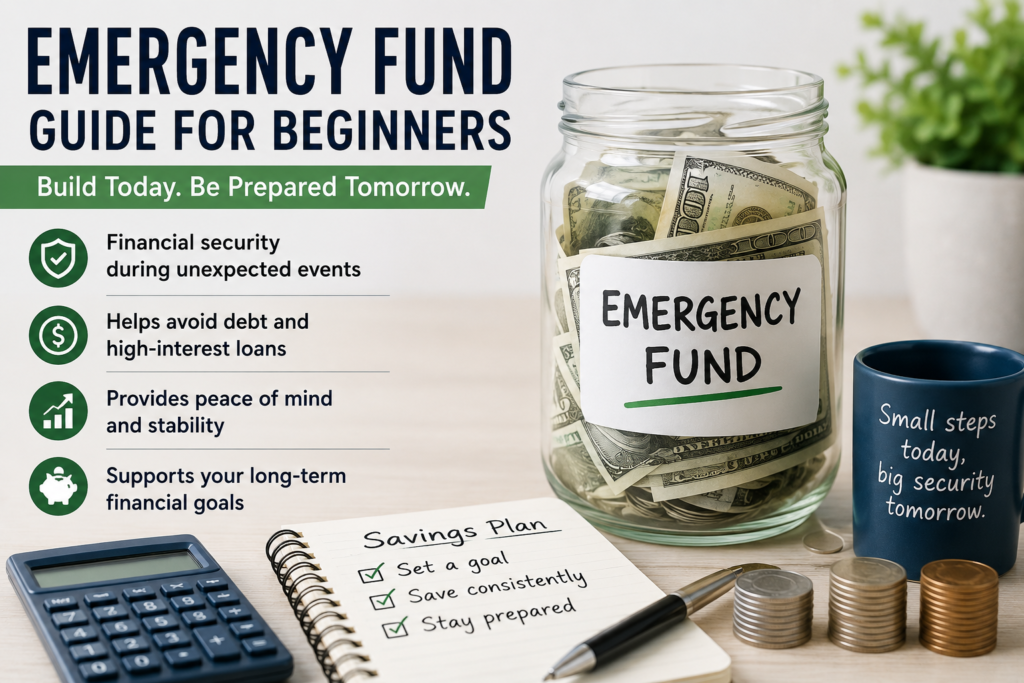

An emergency fund serves as a financial safety net designed to help you manage unforeseen expenses without disrupting your long-term financial goals. Building an emergency fund may seem challenging at first, especially if you’re living on a tight budget, but even small contributions can make a meaningful difference over time.

This guide explains what an emergency fund is, why it matters, how much you should save, and practical steps to help you build financial security.

What Is an Emergency Fund?

An emergency fund is money set aside specifically for unexpected financial emergencies.

Examples include:

- Medical emergencies

- Job loss or reduced income

- Emergency travel expenses

- Vehicle repairs

- Home repairs

- Unexpected family expenses

An emergency fund is not intended for planned purchases such as vacations, entertainment, or holiday shopping.

Its primary purpose is to provide financial protection during difficult situations.

Why Is an Emergency Fund Important?

Many households experience unexpected expenses each year. Without emergency savings, these situations can quickly become stressful and expensive.

Benefits of an emergency fund include:

Financial Stability

Savings provide immediate access to funds when unexpected costs arise.

Reduced Debt

Emergency funds help avoid reliance on high-interest credit cards or personal loans.

Peace of Mind

Knowing you have financial reserves can reduce anxiety during uncertain times.

Greater Financial Flexibility

Emergency savings can help you make better decisions during difficult circumstances instead of reacting under financial pressure.

How Much Should You Save?

There is no universal amount that works for everyone.

The ideal emergency fund depends on your:

- Income

- Living expenses

- Employment stability

- Family responsibilities

- Financial goals

Beginner Goal: $500 to $1,000

For many people, the first milestone is saving enough to cover smaller emergencies.

Examples:

- Vehicle repairs

- Minor medical bills

- Appliance replacement

Intermediate Goal: Three Months of Expenses

Many financial professionals recommend saving enough to cover approximately three months of essential living expenses.

Long-Term Goal: Six Months or More

Individuals with variable income, self-employment income, or significant family responsibilities may choose to save six months or more of essential expenses.

Step 1: Calculate Your Essential Monthly Expenses

Begin by identifying your core monthly expenses.

Examples include:

- Housing

- Utilities

- Groceries

- Transportation

- Insurance

- Healthcare

- Debt payments

Example

Rent: $1,200

Utilities: $200

Groceries: $400

Transportation: $300

Insurance: $150

Total essential expenses: $2,250

Three months of expenses would equal approximately $6,750.

Step 2: Set a Realistic Savings Goal

Large savings targets can feel overwhelming.

Instead, break your goal into smaller milestones.

Example

Goal 1: $500

Goal 2: $1,000

Goal 3: One month of expenses

Goal 4: Three months of expenses

Goal 5: Six months of expenses

Achieving smaller goals creates motivation and builds momentum.

Step 3: Create a Monthly Savings Plan

Consistency is more important than the amount.

Even small contributions can grow over time.

Example Monthly Contributions

$25 per week = $1,300 annually

$50 per week = $2,600 annually

$100 per week = $5,200 annually

The key is making saving a regular habit.

Step 4: Automate Your Savings

Automation helps remove the temptation to spend money before saving it.

Consider:

- Automatic bank transfers

- Payroll deductions

- Automatic savings deposits

Treat emergency savings as a regular monthly expense.

Step 5: Reduce Unnecessary Spending

Finding additional money for savings often requires reviewing spending habits.

Possible areas to reduce:

- Unused subscriptions

- Dining out expenses

- Impulse purchases

- Entertainment costs

- Premium services you rarely use

Small reductions can significantly increase savings over time.

Where Should You Keep Your Emergency Fund?

Your emergency savings should be:

Easily Accessible

You should be able to access funds quickly during emergencies.

Safe

Emergency funds are designed for security rather than investment growth.

Separate From Everyday Spending

Keeping savings separate can reduce the temptation to spend the money.

Common options include:

- Savings accounts

- High-yield savings accounts

- Money market accounts

Common Emergency Fund Mistakes

Waiting Until You Earn More

Many people delay saving because they believe they need a higher income.

Starting small is often more effective than waiting.

Using Emergency Savings for Non-Emergencies

Avoid using the fund for:

- Vacations

- Electronics

- Luxury purchases

- Entertainment

Keeping Savings Mixed With Spending Accounts

Separate accounts can help maintain discipline.

Ignoring Inflation and Lifestyle Changes

Review your savings goals periodically as expenses change.

Emergency Fund Strategies for Different Situations

Employees

Aim for three to six months of essential expenses.

Self-Employed Individuals

Consider maintaining six to twelve months of expenses due to income variability.

Families

Households with dependents often benefit from larger emergency reserves.

Retirees

Emergency savings can help cover unexpected healthcare or home maintenance expenses.

Practical Tips for Faster Savings Growth

- Save tax refunds

- Save bonuses

- Redirect pay raises

- Sell unused items

- Use cashback rewards responsibly

- Review spending monthly

Every contribution helps strengthen your financial foundation.

Frequently Asked Questions

How much should a beginner save first?

Many beginners aim for an initial emergency fund of $500 to $1,000.

How long does it take to build an emergency fund?

The timeline depends on your income, expenses, and savings rate. Consistent contributions can help build savings steadily over time.

Should I invest my emergency fund?

Emergency funds are generally intended for stability and accessibility rather than investment growth.

Can I build an emergency fund while paying off debt?

Many people choose to build a small emergency fund first while continuing debt repayment efforts.

What qualifies as a financial emergency?

Unexpected expenses such as medical bills, job loss, essential home repairs, or vehicle repairs typically qualify as emergencies.

Conclusion

An emergency fund is one of the most important components of a healthy financial plan. It provides protection against unexpected expenses, reduces reliance on debt, and offers greater peace of mind during uncertain times.

Building an emergency fund does not require large amounts of money at the beginning. By starting small, saving consistently, and maintaining clear financial goals, you can gradually create a financial safety net that supports long-term stability and confidence.

The most important step is simply getting started today.

Sources

- Consumer Financial Protection Bureau (CFPB)

- Federal Trade Commission (FTC)

- FDIC Consumer Resources

- Public financial literacy resources

About the Author

Elizabeth Toohey

Elizabeth Toohey is a personal finance researcher and content writer specializing in budgeting, savings strategies, consumer banking, and financial literacy. She focuses on creating educational content that helps readers better understand everyday money management, financial planning, and responsible borrowing practices.

{kind=link}